Attaching package: 'ISLR2'The following object is masked from 'package:MASS':

BostonIntroduction to Statistical Learning - PISE

library() loads packagesRRMASSISLR2

Attaching package: 'ISLR2'The following object is masked from 'package:MASS':

Bostonlibrary() returns an errorMASS) usually come with RISLR2) may need to be installed firstinstall.packages("ISLR2")R session with library()Boston is a dataset in ISLR2medv (median house value)rmagelstat crim zn indus chas nox rm age dis rad tax ptratio lstat medv

1 0.00632 18 2.31 0 0.538 6.575 65.2 4.0900 1 296 15.3 4.98 24.0

2 0.02731 0 7.07 0 0.469 6.421 78.9 4.9671 2 242 17.8 9.14 21.6

3 0.02729 0 7.07 0 0.469 7.185 61.1 4.9671 2 242 17.8 4.03 34.7

4 0.03237 0 2.18 0 0.458 6.998 45.8 6.0622 3 222 18.7 2.94 33.4

5 0.06905 0 2.18 0 0.458 7.147 54.2 6.0622 3 222 18.7 5.33 36.2

6 0.02985 0 2.18 0 0.458 6.430 58.7 6.0622 3 222 18.7 5.21 28.7Use ?Boston to see the dataset documentation

Fit a simple linear regression with lm()

Syntax: lm(y ~ x, data = dataset)

Here:

medvlstatR does not know where medv and lstat are storeddata = Boston, orattach(Boston)lm.fit gives basic model outputsummary(lm.fit) gives more details:

Call:

lm(formula = medv ~ lstat)

Coefficients:

(Intercept) lstat

34.55 -0.95

Call:

lm(formula = medv ~ lstat)

Residuals:

Min 1Q Median 3Q Max

-15.168 -3.990 -1.318 2.034 24.500

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 34.55384 0.56263 61.41 <2e-16 ***

lstat -0.95005 0.03873 -24.53 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 6.216 on 504 degrees of freedom

Multiple R-squared: 0.5441, Adjusted R-squared: 0.5432

F-statistic: 601.6 on 1 and 504 DF, p-value: < 2.2e-16names() to see what is stored in the fitted model objectcoef() to access components safely [1] "coefficients" "residuals" "effects" "rank"

[5] "fitted.values" "assign" "qr" "df.residual"

[9] "xlevels" "call" "terms" "model" (Intercept) lstat

34.5538409 -0.9500494 confint() to compute confidence intervals for coefficientspredict() to compute:

fit lwr upr

1 29.80359 29.00741 30.59978

2 25.05335 24.47413 25.63256

3 20.30310 19.73159 20.87461 fit lwr upr

1 29.80359 17.565675 42.04151

2 25.05335 12.827626 37.27907

3 20.30310 8.077742 32.52846Confidence and prediction intervals are centered at the same fitted value

Prediction intervals are wider than confidence intervals

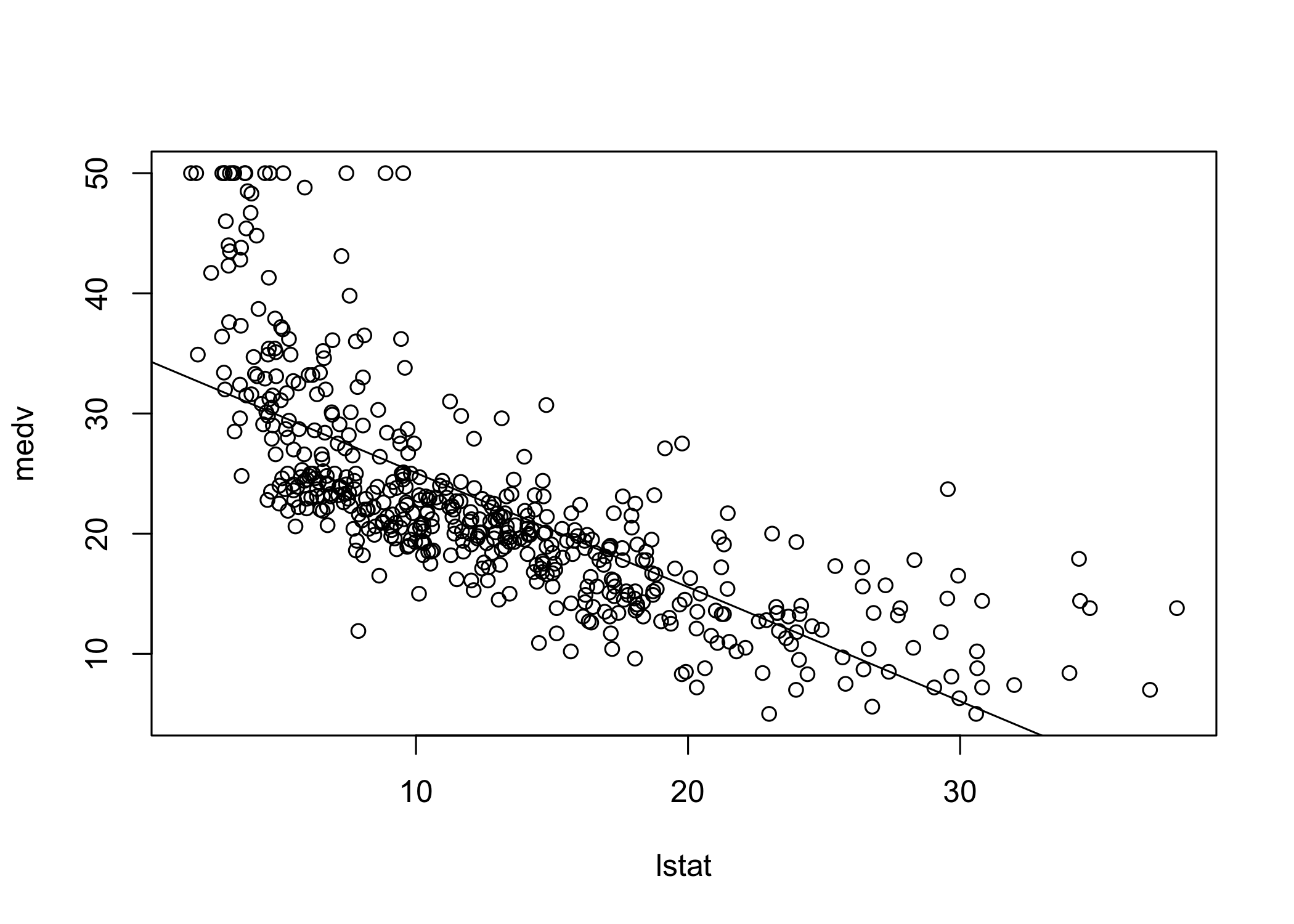

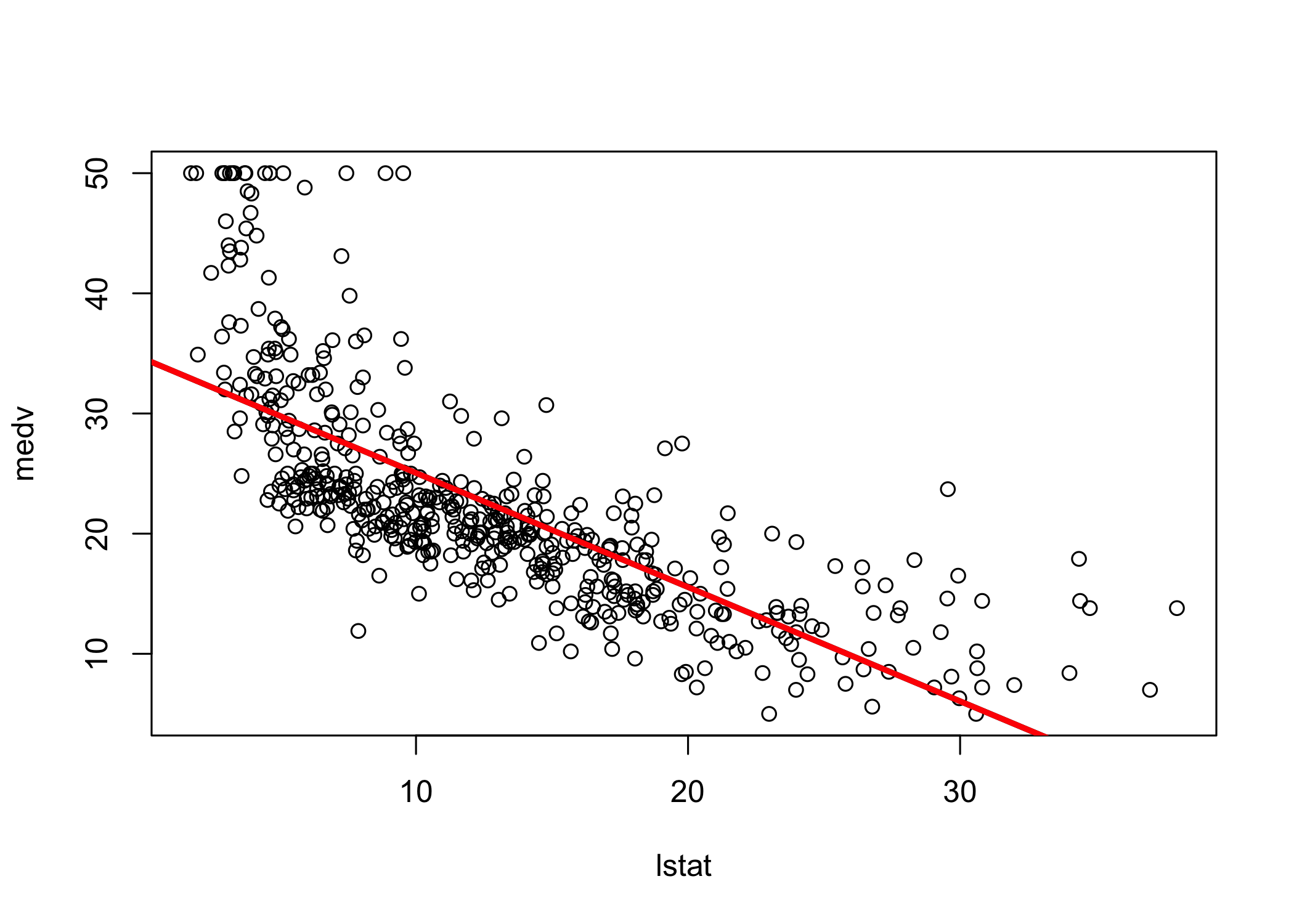

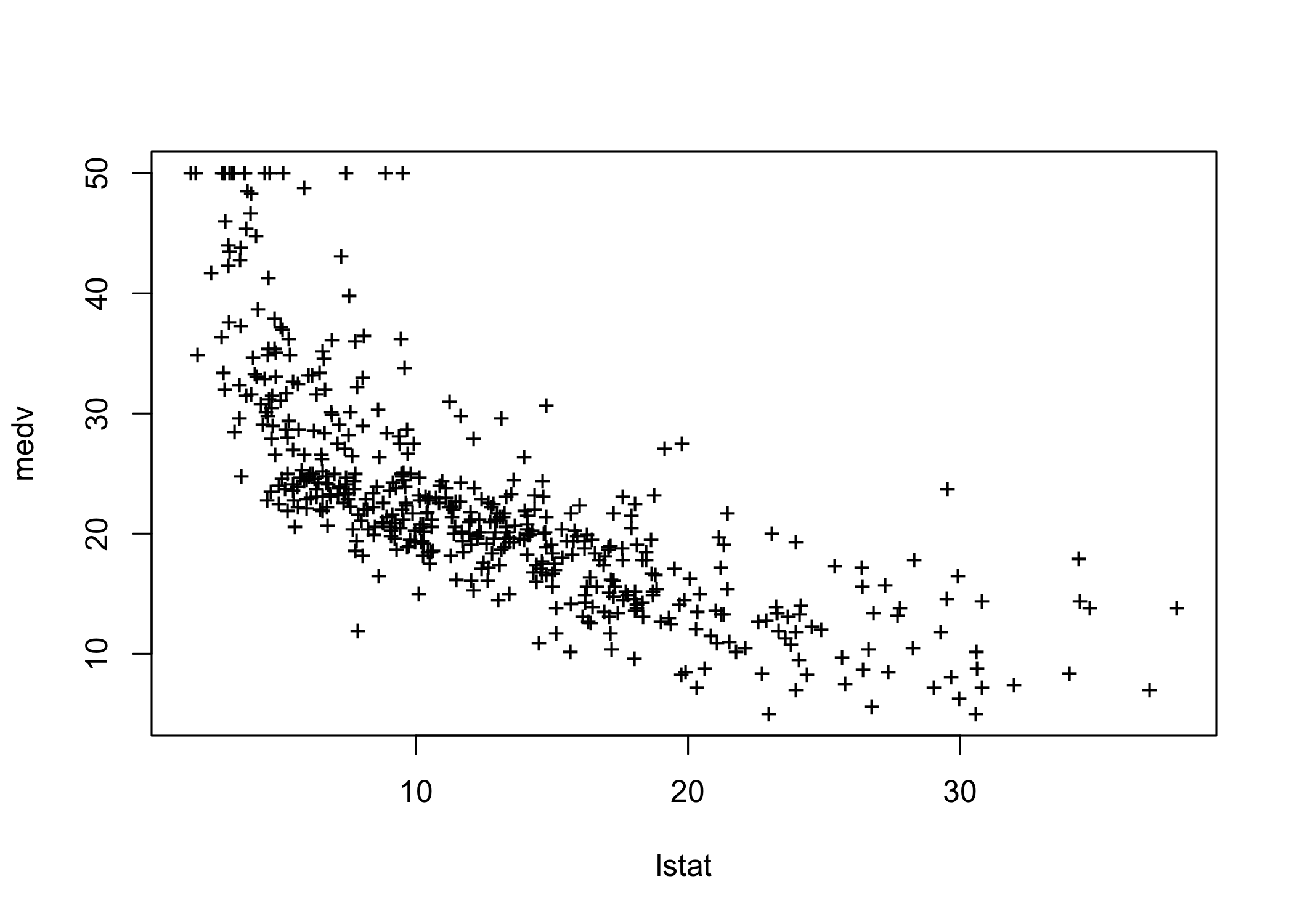

Plot the data and add the least-squares regression line

The plot suggests some possible non-linearity

We will revisit this later

abline() can add any line to a plot

abline(a, b) draws a line with:

abPlot options:

lwd controls line widthcol controls colorpch controls plotting symbollm() can include transformed predictorsI() when arithmetic operators would otherwise be interpreted specially in a formulaI(lstat^2) adds a quadratic term

Call:

lm(formula = medv ~ lstat + I(lstat^2), data = Boston)

Residuals:

Min 1Q Median 3Q Max

-15.2834 -3.8313 -0.5295 2.3095 25.4148

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 42.862007 0.872084 49.15 <2e-16 ***

lstat -2.332821 0.123803 -18.84 <2e-16 ***

I(lstat^2) 0.043547 0.003745 11.63 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 5.524 on 503 degrees of freedom

Multiple R-squared: 0.6407, Adjusted R-squared: 0.6393

F-statistic: 448.5 on 2 and 503 DF, p-value: < 2.2e-16anova()Analysis of Variance Table

Model 1: medv ~ lstat

Model 2: medv ~ lstat + I(lstat^2)

Res.Df RSS Df Sum of Sq F Pr(>F)

1 504 19472

2 503 15347 1 4125.1 135.2 < 2.2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1Model 1: linear fit with lstat

Model 2: quadratic fit with lstat and lstat^2

anova() tests whether the larger model improves fit significantly

Very small p-value indicates strong evidence in favor of the quadratic model

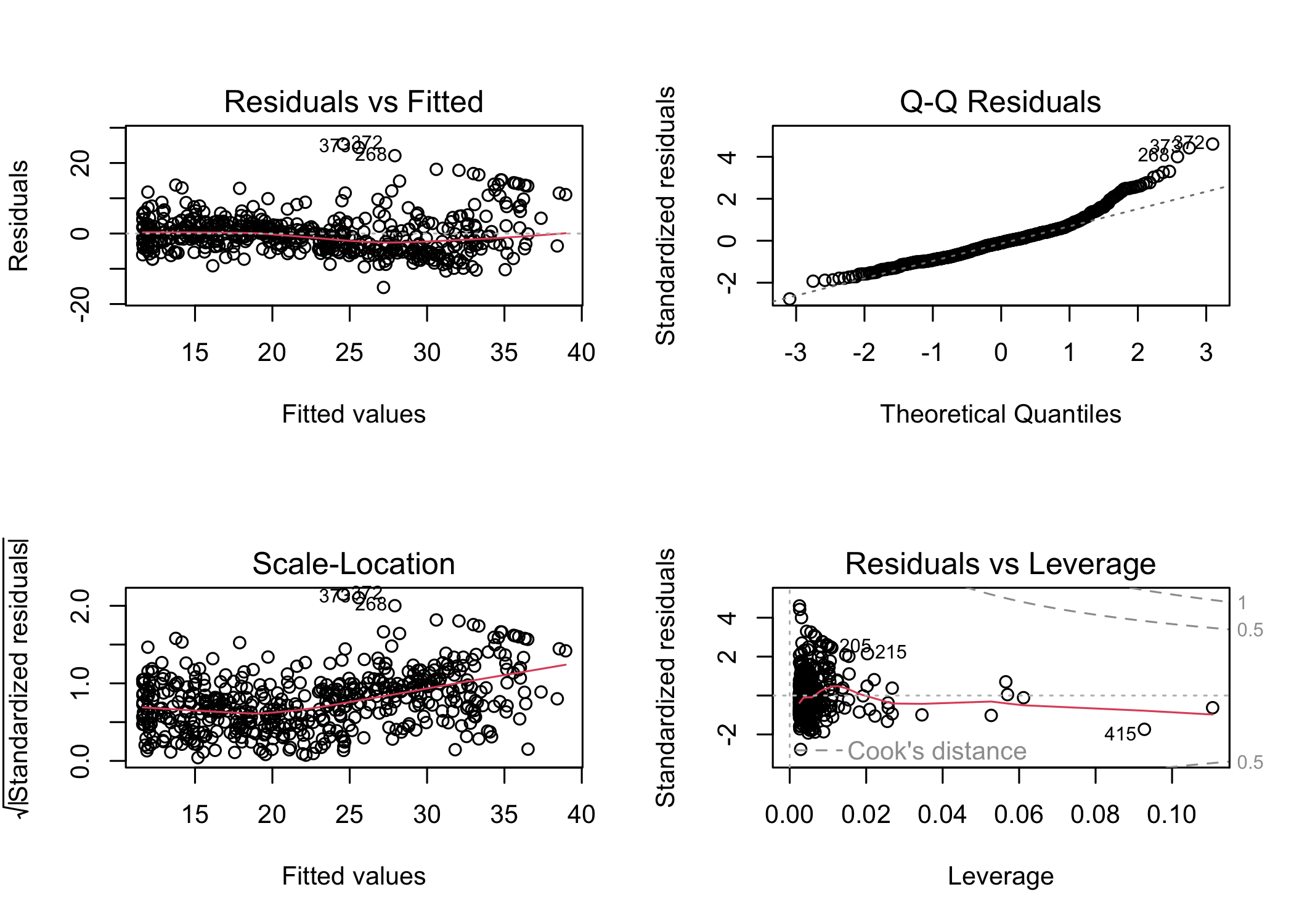

Check the residual diagnostics for the quadratic model

With the quadratic term included, residual patterns are reduced

For higher-order polynomials, poly() is more convenient than writing each power manually

Example: fifth-order polynomial fit

Call:

lm(formula = medv ~ poly(lstat, 5), data = Boston)

Residuals:

Min 1Q Median 3Q Max

-13.5433 -3.1039 -0.7052 2.0844 27.1153

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 22.5328 0.2318 97.197 < 2e-16 ***

poly(lstat, 5)1 -152.4595 5.2148 -29.236 < 2e-16 ***

poly(lstat, 5)2 64.2272 5.2148 12.316 < 2e-16 ***

poly(lstat, 5)3 -27.0511 5.2148 -5.187 3.10e-07 ***

poly(lstat, 5)4 25.4517 5.2148 4.881 1.42e-06 ***

poly(lstat, 5)5 -19.2524 5.2148 -3.692 0.000247 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 5.215 on 500 degrees of freedom

Multiple R-squared: 0.6817, Adjusted R-squared: 0.6785

F-statistic: 214.2 on 5 and 500 DF, p-value: < 2.2e-16Higher-order polynomial terms can improve fit

In this example, terms beyond fifth order are not significant

By default, poly() uses orthogonal polynomials

These are not the raw powers of the predictor

Fitted values are the same as with raw polynomials, but coefficients differ

Use raw = TRUE if raw powers are desired

We are not restricted to polynomial transformations

Example: log transformation

Call:

lm(formula = medv ~ log(rm), data = Boston)

Residuals:

Min 1Q Median 3Q Max

-19.487 -2.875 -0.104 2.837 39.816

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -76.488 5.028 -15.21 <2e-16 ***

log(rm) 54.055 2.739 19.73 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 6.915 on 504 degrees of freedom

Multiple R-squared: 0.4358, Adjusted R-squared: 0.4347

F-statistic: 389.3 on 1 and 504 DF, p-value: < 2.2e-16Auto data settrain contains the indices of the training observationssubset = trainpredict() to compute fitted values for all observations-train selects the validation observationspoly() to fit polynomial regressionslm.fit2 <- lm(mpg ~ poly(horsepower, 2), data = Auto,

subset = train)

mean((mpg - predict(lm.fit2, Auto))[-train]^2)[1] 18.71646lm.fit3 <- lm(mpg ~ poly(horsepower, 3), data = Auto,

subset = train)

mean((mpg - predict(lm.fit3, Auto))[-train]^2)[1] 18.79401set.seed(2)

train <- sample(392, 196)

lm.fit <- lm(mpg ~ horsepower, subset = train)

mean((mpg - predict(lm.fit, Auto))[-train]^2)[1] 25.72651lm.fit2 <- lm(mpg ~ poly(horsepower, 2), data = Auto,

subset = train)

mean((mpg - predict(lm.fit2, Auto))[-train]^2)[1] 20.43036lm.fit3 <- lm(mpg ~ poly(horsepower, 3), data = Auto,

subset = train)

mean((mpg - predict(lm.fit3, Auto))[-train]^2)[1] 20.38533cv.glm()cv.glm() works with models fit using glm()family argument, glm() performs linear regressionglm() and lm() give the same fit here(Intercept) horsepower

39.9358610 -0.1578447 (Intercept) horsepower

39.9358610 -0.1578447 glm() because it works with cv.glm()cv.glm() is in the boot packagelibrary(boot)

glm.fit <- glm(mpg ~ horsepower, data = Auto)

cv.err <- cv.glm(Auto, glm.fit)

cv.err$delta[1] 24.23151 24.23114cv.glm() returns a list

delta contains the cross-validation estimates

For LOOCV, the two values are essentially the same

Compute LOOCV error for polynomial models of degree 1 to 10

Store the results in a vector

cv.error <- rep(0, 10)

for (i in 1:10) {

glm.fit <- glm(mpg ~ poly(horsepower, i), data = Auto)

cv.error[i] <- cv.glm(Auto, glm.fit)$delta[1]

}

cv.error [1] 24.23151 19.24821 19.33498 19.42443 19.03321 18.97864 18.83305 18.96115

[9] 19.06863 19.49093cv.glm() can also perform k-fold CVset.seed(17)

cv.error.10 <- rep(0, 10)

for (i in 1:10) {

glm.fit <- glm(mpg ~ poly(horsepower, i), data = Auto)

cv.error.10[i] <- cv.glm(Auto, glm.fit, K = 10)$delta[1]

}

cv.error.10 [1] 24.27207 19.26909 19.34805 19.29496 19.03198 18.89781 19.12061 19.14666

[9] 18.87013 20.95520delta are almost identical