Lab 4

Decision Trees, Bagging, Random Forests, and Boosting

Decision Trees

Fitting Classification Trees

- The

treelibrary in R is used to construct regression trees

- Fit a regression tree using the

Bostondataset

- Split data into a training set

- Train the tree model on the training data

library(MASS)

set.seed(1)

train <- sample(1:nrow(Boston), nrow(Boston) / 2)

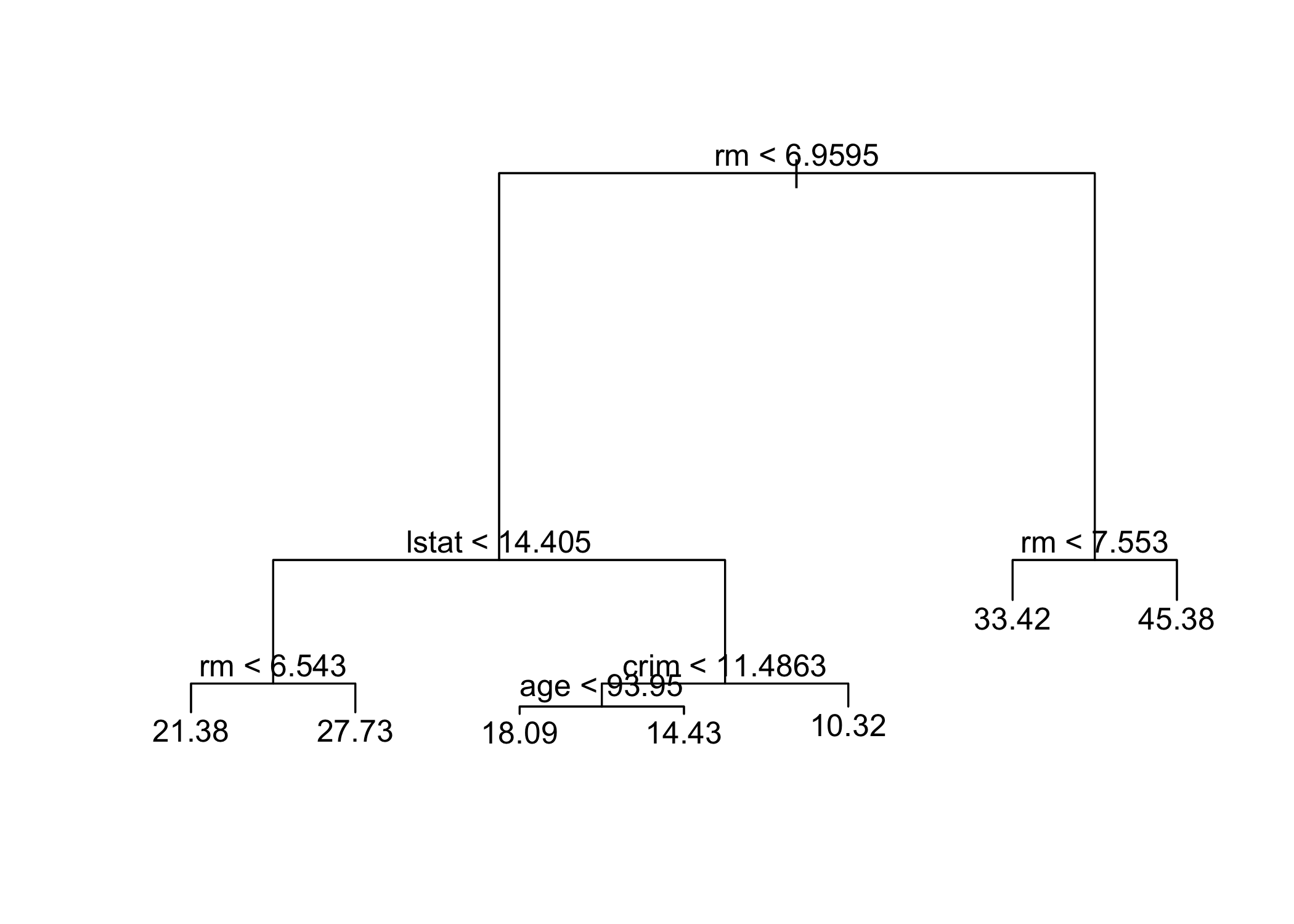

tree.boston <- tree(medv ~ ., Boston, subset = train)

summary(tree.boston)

Regression tree:

tree(formula = medv ~ ., data = Boston, subset = train)

Variables actually used in tree construction:

[1] "rm" "lstat" "crim" "age"

Number of terminal nodes: 7

Residual mean deviance: 10.38 = 2555 / 246

Distribution of residuals:

Min. 1st Qu. Median Mean 3rd Qu. Max.

-10.1800 -1.7770 -0.1775 0.0000 1.9230 16.5800 summary()shows only 4 variables are used in the tree

- In regression trees, deviance = sum of squared errors (SSE)

lstat: % of lower socioeconomic status

rm: average number of roomsInterpretation:

- Higher

rm→ higher house prices

- Lower

lstat→ higher house prices

- Example:

rm ≥ 7.553→ predicted price ≈ $45,400

- Higher

Model flexibility:

- Larger tree can be grown using

tree.control(..., mindev = 0)

- Larger tree can be grown using

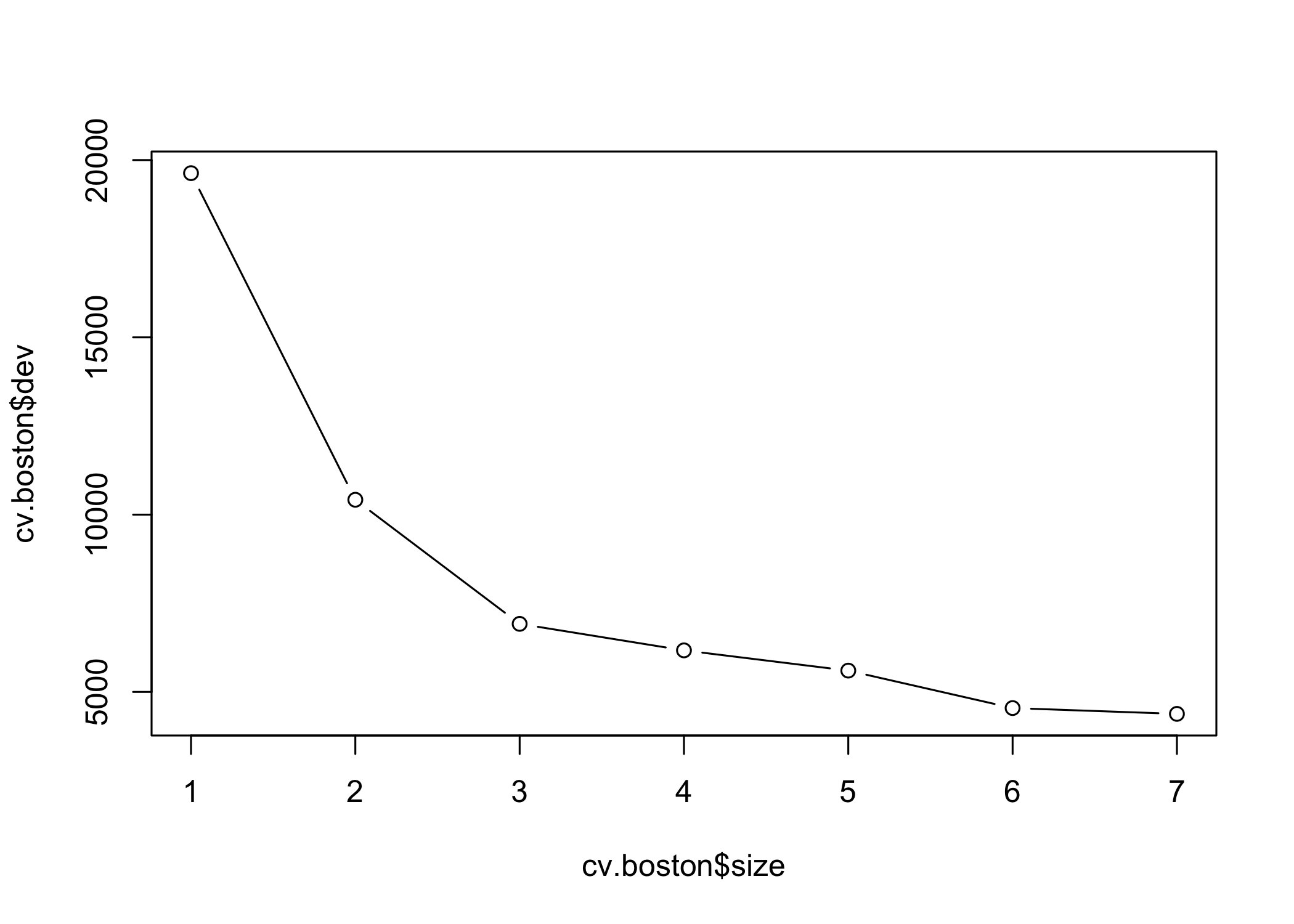

Next step:

- Use

cv.tree()to evaluate pruning via cross-validation

- Use

- Cross-validation selects the most complex tree in this case

- Tree can still be pruned manually if desired

- Based on cross-validation, the unpruned tree is selected

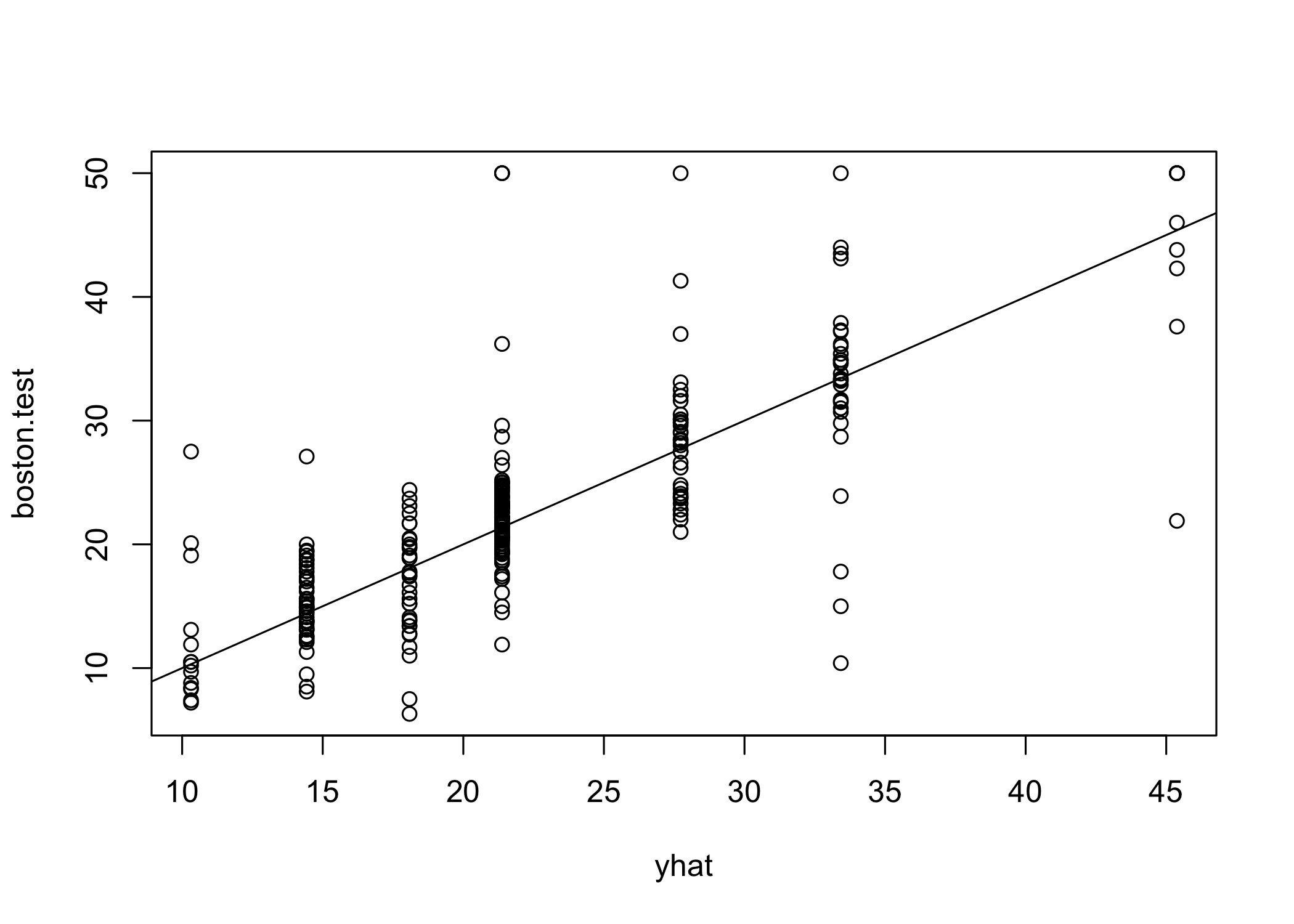

- Use the unpruned tree to make predictions on the test set

yhat <- predict(tree.boston, newdata = Boston[-train, ])

boston.test <- Boston[-train, "medv"]

plot(yhat, boston.test)

abline(0, 1)

[1] 35.28688- Test set MSE ≈ 35.29

- RMSE ≈ 5.941

- Predictions are on average within ~$5,941 of true median house values

Bagging and Random Forests

- Apply bagging and random forests using the

randomForestpackage in R

- Bagging = special case of random forest with m = p (all predictors used at each split)

randomForest 4.7-1.1Type rfNews() to see new features/changes/bug fixes.set.seed(1)

bag.boston <- randomForest(medv ~ ., data = Boston,

subset = train, mtry = 12, importance = TRUE)

bag.boston

Call:

randomForest(formula = medv ~ ., data = Boston, mtry = 12, importance = TRUE, subset = train)

Type of random forest: regression

Number of trees: 500

No. of variables tried at each split: 12

Mean of squared residuals: 11.10176

% Var explained: 85.56mtry = 12→ all 12 predictors used at each split

- This corresponds to bagging

- Evaluate model performance on the test set

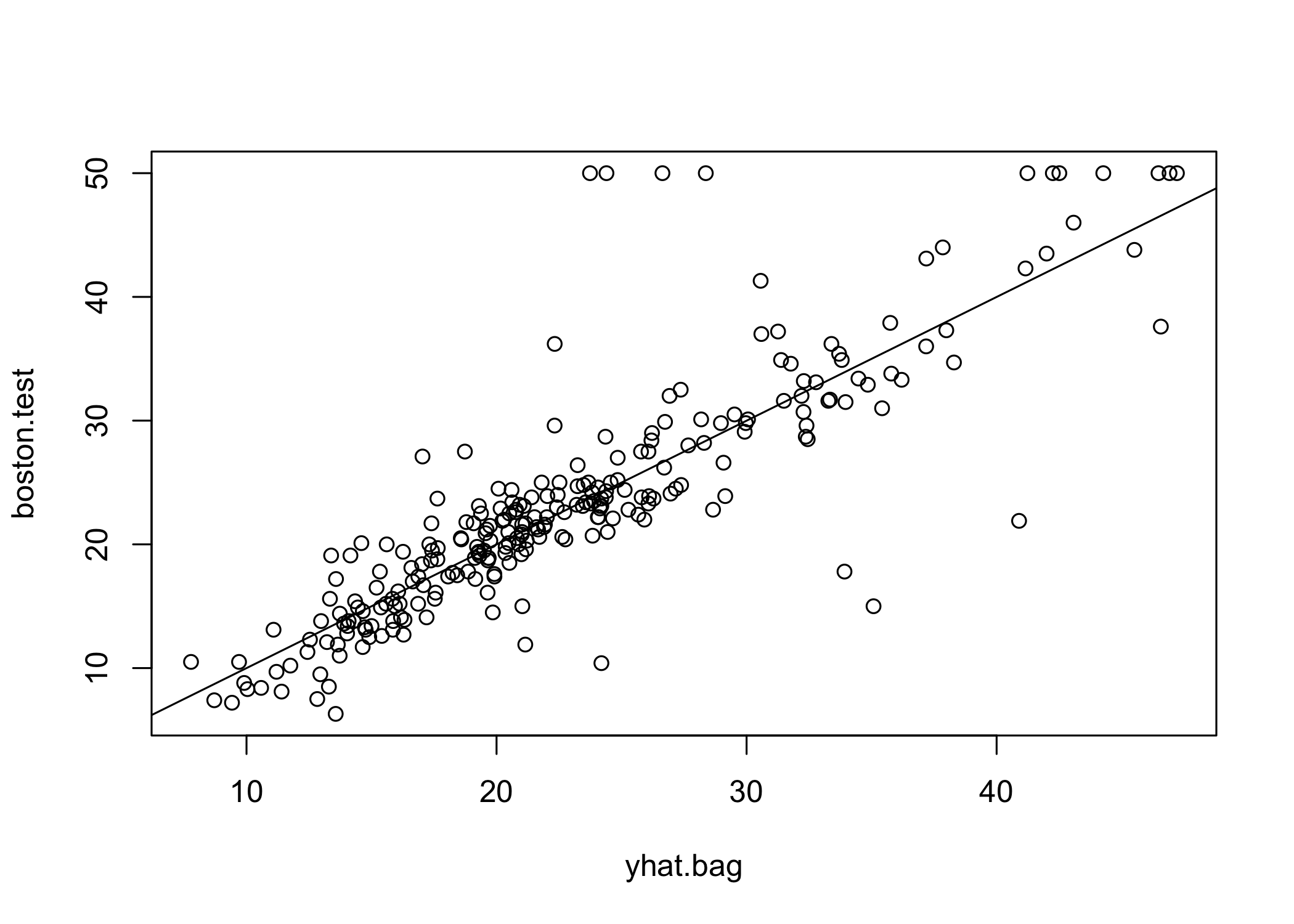

yhat.bag <- predict(bag.boston, newdata = Boston[-train, ])

plot(yhat.bag, boston.test)

abline(0, 1)

[1] 23.38773- Bagged model test MSE ≈ 23.42

- Significantly lower than single tree (~2/3 of its error)

- Number of trees can be controlled with the

ntreeparameter

bag.boston <- randomForest(medv ~ ., data = Boston,

subset = train, mtry = 12, ntree = 25)

yhat.bag <- predict(bag.boston, newdata = Boston[-train, ])

mean((yhat.bag - boston.test)^2)[1] 25.19144- Random forests are built like bagging but with smaller

mtry

- Default

mtry:- Regression: p/3

- Here,

mtry = 6is used

set.seed(1)

rf.boston <- randomForest(medv ~ ., data = Boston,

subset = train, mtry = 6, importance = TRUE)

yhat.rf <- predict(rf.boston, newdata = Boston[-train, ])

mean((yhat.rf - boston.test)^2)[1] 19.62021- Random forest test MSE ≈ 20.07

- Improves over bagging performance

- Use

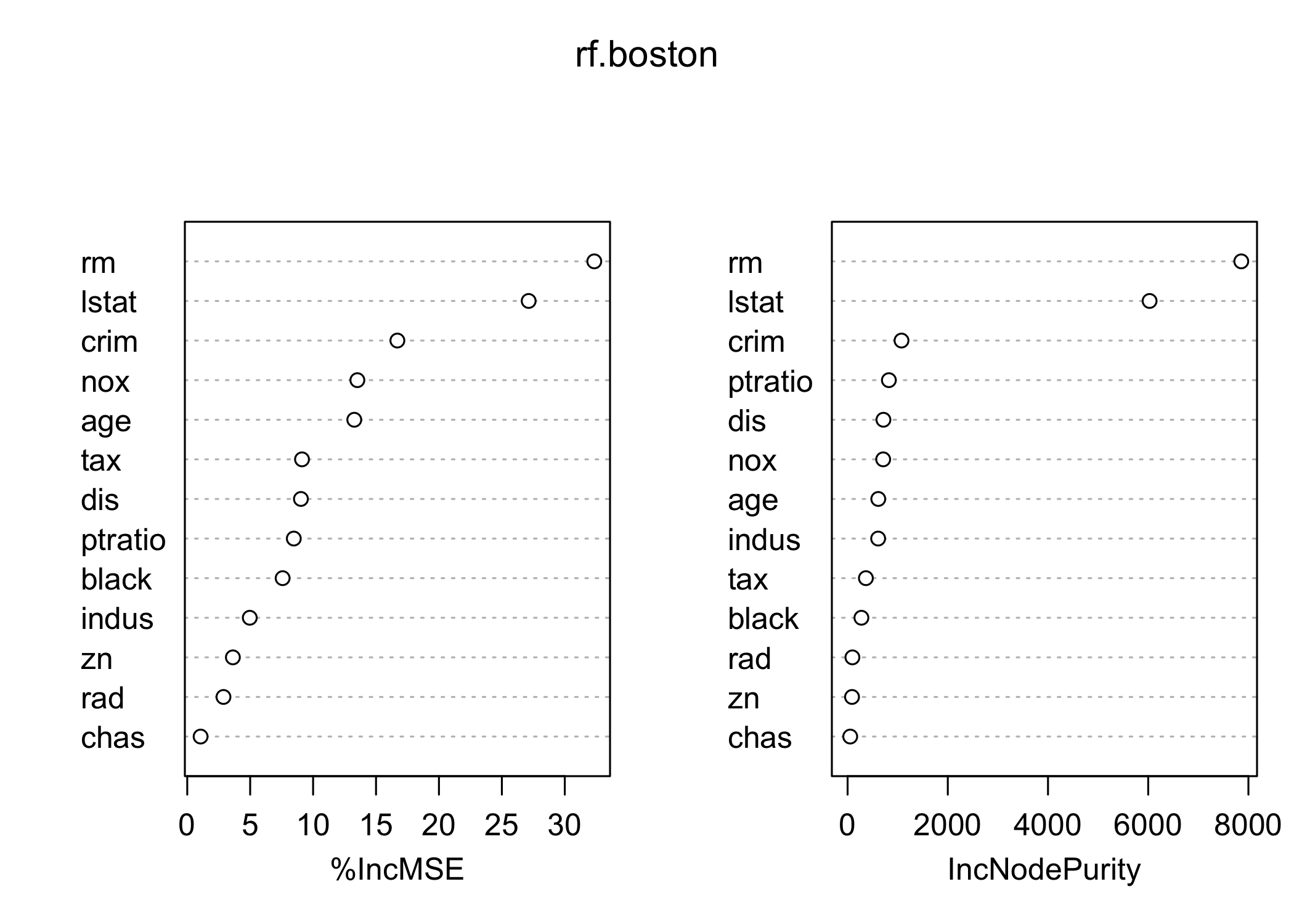

importance()to evaluate variable importance

%IncMSE IncNodePurity

crim 16.697017 1076.08786

zn 3.625784 88.35342

indus 4.968621 609.53356

chas 1.061432 52.21793

nox 13.518179 709.87339

rm 32.343305 7857.65451

age 13.272498 612.21424

dis 9.032477 714.94674

rad 2.878434 95.80598

tax 9.118801 364.92479

ptratio 8.467062 823.93341

black 7.579482 275.62272

lstat 27.129817 6027.63740- Two measures of variable importance:

- Mean decrease in accuracy (via permutation on out-of-bag samples)

- Mean decrease in node impurity (averaged over all trees)

- Most important variables in the random forest:

lstat(wealth / socioeconomic status)

rm(house size / number of rooms)

Boosting

- Use the

gbmpackage to fit boosted regression trees

- Apply

gbm()to theBostondataset

- Set

distribution = "gaussian"for regression problems

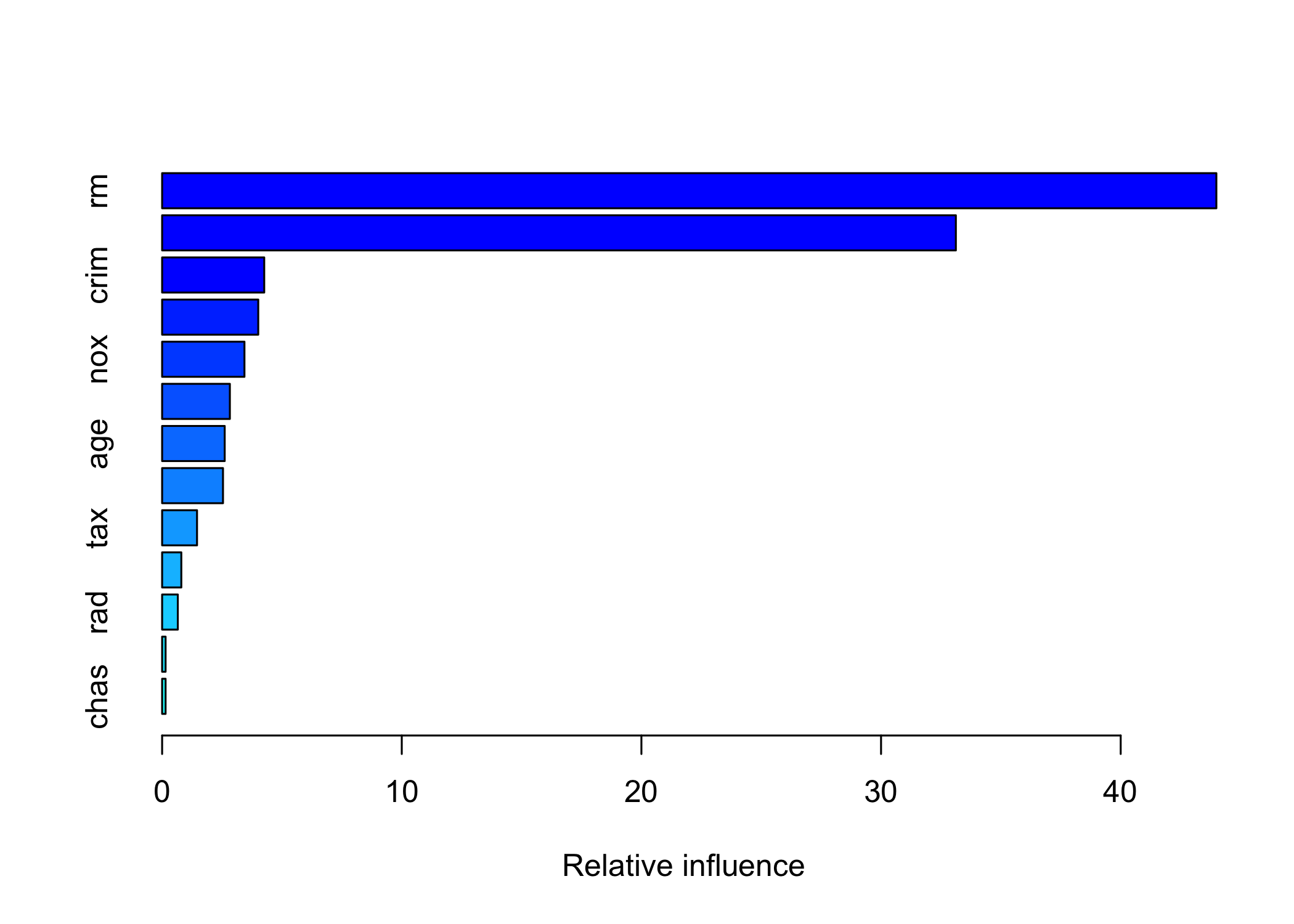

Loaded gbm 2.2.2This version of gbm is no longer under development. Consider transitioning to gbm3, https://github.com/gbm-developers/gbm3summary()provides:- Relative influence plot

- Numerical measures of variable importance

- Relative influence plot

var rel.inf

rm rm 43.9919329

lstat lstat 33.1216941

crim crim 4.2604167

dis dis 4.0111090

nox nox 3.4353017

black black 2.8267554

age age 2.6113938

ptratio ptratio 2.5403035

tax tax 1.4565654

indus indus 0.8008740

rad rad 0.6546400

zn zn 0.1446149

chas chas 0.1443986lstatandrmare the most important variables

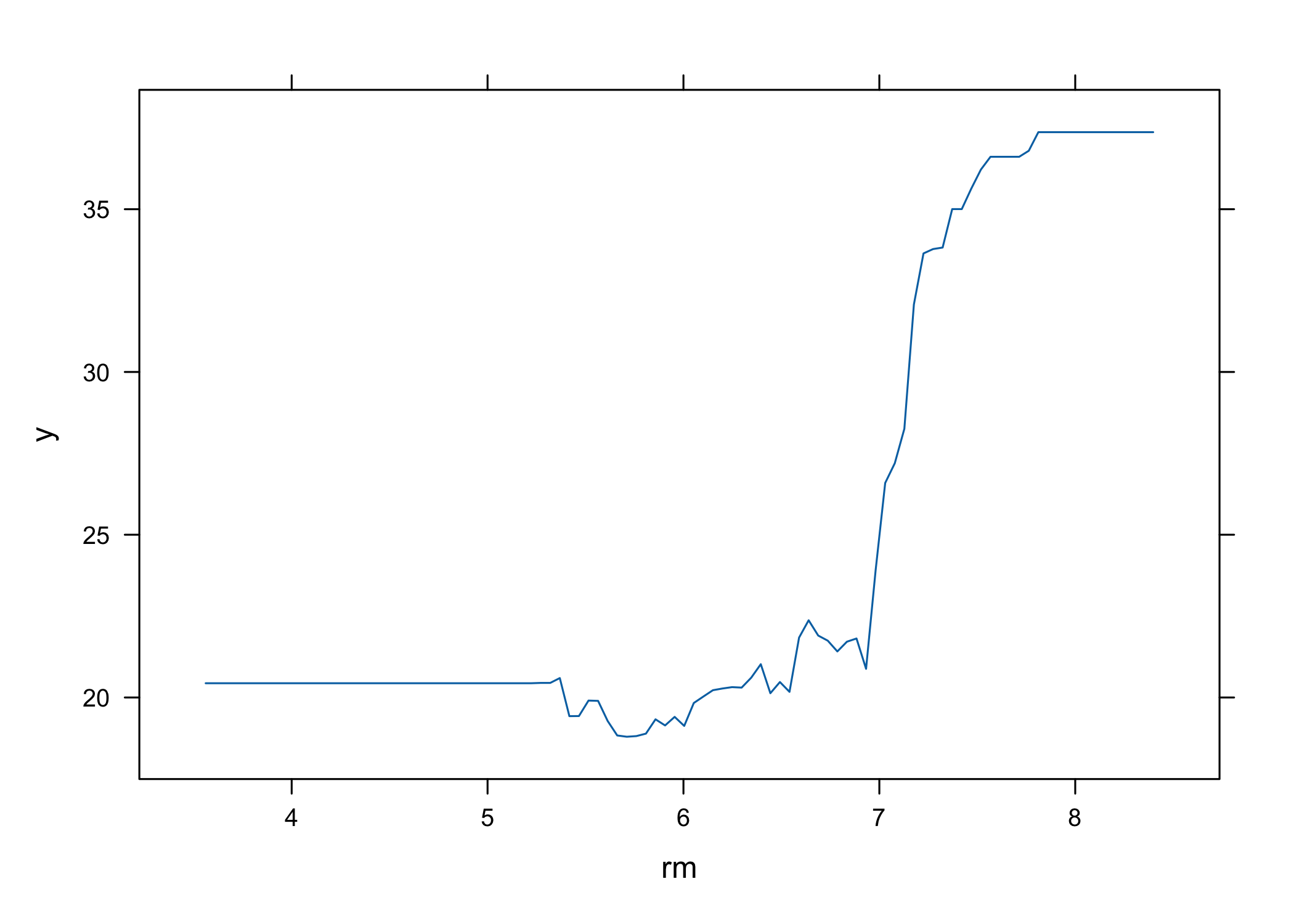

- Partial dependence plots can be generated for these variables

- Partial dependence plots show marginal effect of variables on response

- Effects observed:

- Higher

rm→ higher house prices

- Higher

lstat→ lower house prices

- Higher

- Use boosted model to predict

medvon the test set

yhat.boost <- predict(boost.boston,

newdata = Boston[-train, ], n.trees = 5000)

mean((yhat.boost - boston.test)^2)[1] 18.84709- Boosting test MSE ≈ 18.39

- Outperforms random forests and bagging

- Model can be tuned via shrinkage parameter \lambda

- Example: use \lambda = 0.2

boost.boston <- gbm(medv ~ ., data = Boston[train, ],

distribution = "gaussian", n.trees = 5000,

interaction.depth = 4, shrinkage = 0.2, verbose = FALSE)

yhat.boost <- predict(boost.boston,

newdata = Boston[-train, ], n.trees = 5000)

mean((yhat.boost - boston.test)^2)[1] 18.33455- Using \lambda = 0.2 results in lower test MSE than \lambda = 0.001